Investment Funds Multiplier case study

Investment Funds Multiplier case study

A margin loan exclusive to Leveraged.

The Investment Funds Multiplier may be suitable if you:

- Want to build an investment portfolio over the medium to long term.

- Believe that borrowing to acquire and build your investment portfolio is a suitable strategy for your financial goals and risk appetite.

- Require certainty of a repayment plan (instead of a margin call) if the value of your investment portfolio falls.

What is the Investment Funds Multiplier?

The Investment Funds Multiplier is a margin loan facility through which you can borrow to invest with the added benefit of Repayment Plans (such as Periodic Repayment Plans and Lump Sum Repayment Plans).

The Investment Funds Multiplier allows you to borrow money, in addition to using your own funds, to invest in a variety of Acceptable Investments, including shares, Exchange Traded Funds (ETFs), listed investment companies and managed funds. These are mortgaged to the lender as security for the loan and the amount you owe.

By borrowing to invest (also called gearing or leverage) you can build an investment portfolio larger than you would by using only your own funds. Investors use gearing when they expect the return on their investments to be larger than the cost of borrowing.

Yet it’s worth remembering that if the return on your investment is less than your borrowing costs, you will incur a lower return or larger loss than if you had not borrowed or invested at all.

Repayment Plans

In the event of a significant or sustained fall in the investment portfolio value, investors can progressively reduce the loan borrowed through a Repayment Plan to an acceptable level over time. This gives you certainty about the amount you may have to pay should the value of your portfolio fall, making it easier for you to manage your cash flow. It also gives you time to consider how to respond to market movements. Once the market improves, or your loan amount is reduced to an acceptable level, you can return to paying interest only on your loan.

However, if you don’t meet the Repayment Plan schedule, the Lender may sell all, or part, of the investment portfolio. Circumstances can also arise which may result in you being required to repay some, or all, of your loan at short notice by paying and additional amount into your loan account or selling some, or all, of the mortgaged investment portfolio. Please read the PDS for more information.

IFM Case Study

Sandy contributed $40,000 into a traditional margin loan and borrowed $40,000 to invest the total $80,000 into Fund A, which has a Lending Ratio of 75% assigned to it by the margin lender.

| Portfolio of Fund A | |

| Borrower Contribution | $40,000 |

| Loan (Total amount owing) | $40,000 |

| Market Value | $80,000 |

| Gearing Ratio (Loan/Market value) | 50% |

| Maximum Lending Ratio | 75% |

Now let’s assume that due to market volatility, Fund A falls in value by 42% over time, resulting in Sandy’s portfolio being valued at $46,400 ($80,-000 – 42%). Sandy is now in margin call due to being in excess of the Maximum Lending Ratio (75%) plus Buffer of 10% (see below example) and would be required to inject $5,200 (Total Amount Owing – new Security Value) into the margin loan in cash or by selling enough of her portfolio to equate to $5,200 of cash. Unfortunately, Sandy does not have $5,200 in a bank account so she has no option but to sell her investment in Fund A, which is potentially at a much lower price than she is comfortable selling at.

| Portfolio of Fund A | |

| Market Value (Reduction of 42%) | $46,400 |

| Loan (Total amount owing) | $40,000 |

| Net Equity | $6,400 |

| Maximum Lending Ratio | 75% |

| Gearing Ratio | 86% |

| Security Value (Market Value x 75%) | $34,800 |

| Percentage Buffer | 10% |

| Buffer (Market Value x Percentage Buffer) | $4,640 |

| Security Value + Buffer | $39,440 |

| Margin Call Amount (Security Value - Loan (Total amount owing) | $5,200 |

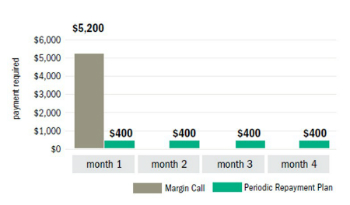

Comparison with and without investment funds multiplier

In this example, if Sandy borrowed through a traditional margin loan, she would be required to make one margin call payment of $5,200. However, if Sandy decided to invest in Fund A using the Investment Funds Multiplier, she will commence a Periodic Repayment Plan of 1% of the Total Amount Owing or $400 per month until the Gearing Ratio is restored to 75%. If we assume the market recovers in 4 months time and Sandy’s Gearing Ratio is restored back to 75%, she would have paid $1600 (4 months x $400) over the period as opposed to one margin call payment of $5200. Sandy would only need to pay a Lump Sum Repayment if the Gearing Ratio were to reach 95%. If this happens, she will have to pay down the loan to an 85% Gearing Ratio so that the Periodic Repayment Plan can continue.

About Leveraged

Established in 1991, we’re proud to be a margin lending specialist in Australia, and a wholly-owned subsidiary of Bendigo and Adelaide Bank.

We offer a choice of multiple margin loan solutions and additional features, a diverse and frequently reviewed investment list and we connect with most major online platforms and selected brokers.

More information

We can help you get started today, complete our enquiry form or call 1300 307 807 to speak to one of our customer service consultants.

Things you should know

Gearing involves risk. It can magnify your returns; however, it may also magnify your losses.

Issued by Leveraged Equities Limited (ABN 26 051 629 282 AFSL 360118) as Lender and as a subsidiary of Bendigo and Adelaide Bank Limited (ABN 11 068 049 178 AFSL 237879). This information is correct as at 03/07/2025. This contains general advice only and doesn’t take into account your personal objectives, financial situation or needs. This information must not be relied upon as a substitute for financial planning, legal, tax or other professional advice. The examples are for illustration purposes only and do not indicate any view of, or expectation about the Investment Funds Multiplier or any investment or transaction. They do not cover all the possible outcomes and are not intended as a recommendation, are simplified and may not reflect actual outcomes, market prices or movements or taxation treatment. Please consider your personal circumstances, consult a professional investment adviser and read the Product Disclosure Statement and Incorporated Statements (together, the 'PDS') and Product Guide, together with the terms and conditions applying to the product or service, available to download from www.leveraged.com.au before making an investment decision. Fees, charges and government taxes may be payable. Lending criteria may apply. Not available for a self-managed superannuation fund. Interest cannot be capitalised and must be paid when due by direct debit. Periodic Repayment Plans are set at 1% of the Total Amount Owing at the time the facility becomes subject to the Periodic Repayment Plan. The Periodic Repayment Plan continues until the Total Amount Owing is less than the prevailing Security Value.